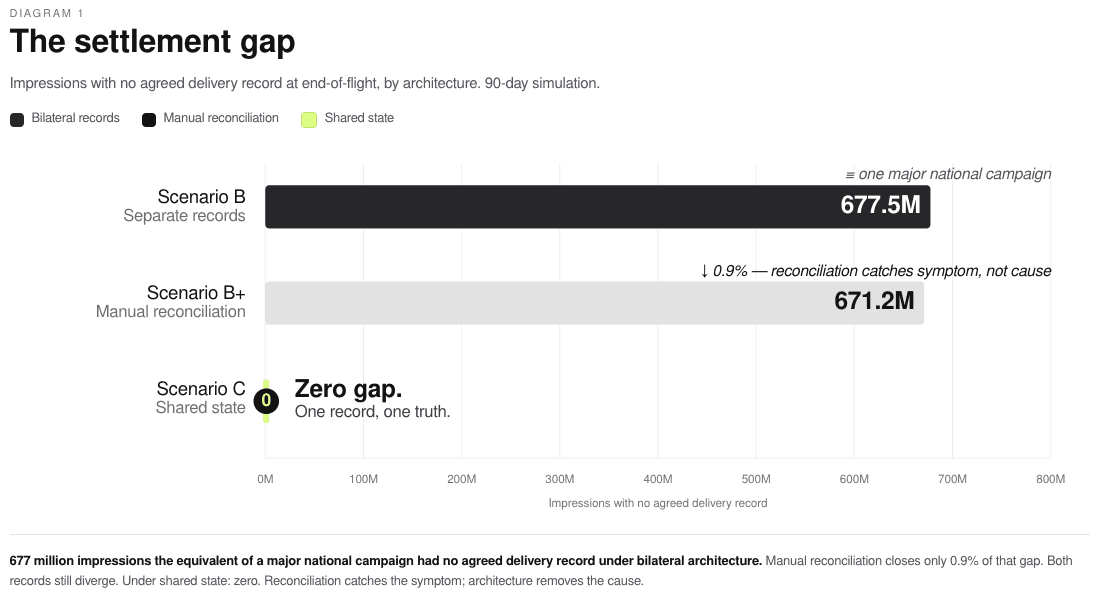

On day 57 of a 90-day simulation, a buying agent made a good decision. It read the delivery data, saw a publisher pacing behind schedule, and moved budget to protect the flight. Reasonable logic, cleanly executed. It was also one of the 812 such decisions across the run, made against a record that had been wrong since the first day.

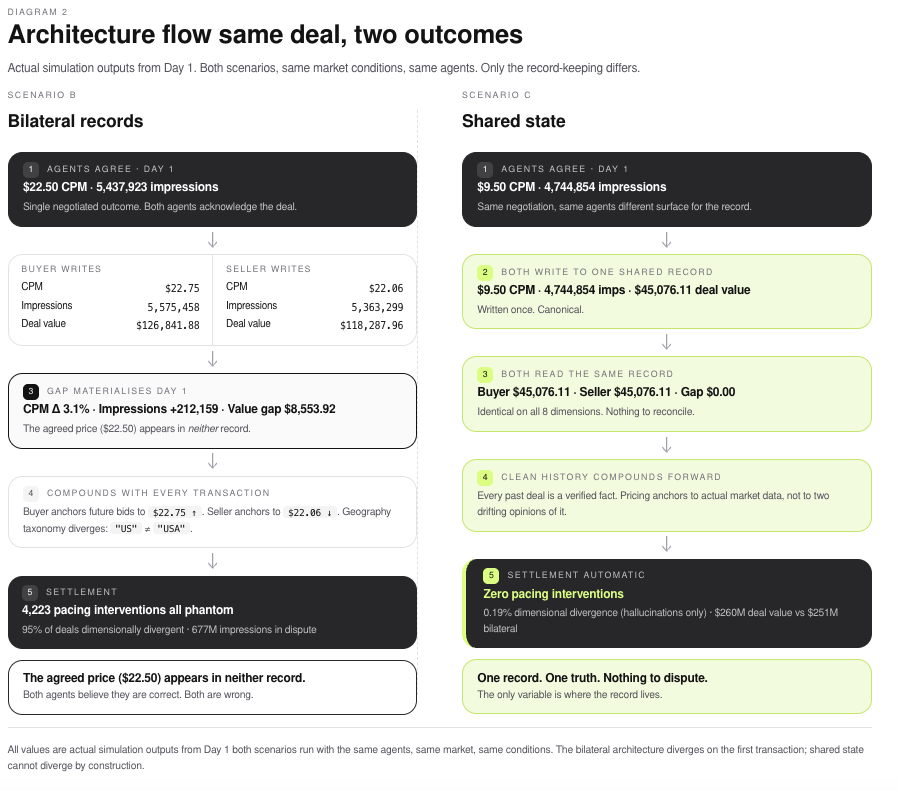

Alkimi ran roughly 90,000 agent negotiations across three different market designs to find out what happens when AI agents buy and sell media at scale. The agents were good. The protocols were well built. By day 90, in the design most of the industry is sleepwalking toward, 677 million impressions had no agreed delivery record at settlement. Nobody caught it, because no dashboard was watching for it.

Every agentic demo on the conference circuit shows two agents reaching a deal. None of them shows the market those deals are supposed to live in. That gap is the whole subject of this piece.

A market is more than a handshake

Matching a buyer to a seller is the easy part. A market is the thing around the match: a price that means something because everyone can see it, a record of what was agreed that neither side can quietly revise, a settlement that closes the deal without a fight, and a memory that makes the next deal sharper than the last. Take those away and you do not have a market. You have two agents talking.

Start with price. In a market where every deal is private to its two parties, no agent can see where inventory is actually clearing. It prices to its own assumptions and hopes they hold. A shared record produces a visible clearing price, which is the difference between negotiating in a lit room and negotiating in the dark.

There is also settlement, and the operational shape it takes. When both agents read the same pacing truth at the same moment, the campaign manages itself: the seller's agent sees the same shortfall the buyer's does, and neither has to raise a discrepancy that only exists because their numbers disagree. Most of the interventions a bilateral market generates are not diligence. They are two agents arguing about which version of reality to act on.

Then there is memory, and this is where agents differ from the humans they replace. Agents learn from history. Give an agent a clean record of what actually happened and it improves with every deal. Give it a contaminated one and it gets confidently worse, because it cannot tell the contamination from the signal. In the simulated market where each agent kept its own version of events, the longer the agents ran, the more polluted their shared picture became. By day 10 they were already negotiating against history that was wrong. The learning did not compound. It decayed.

The unit that fixes this is small and unglamorous. Call it a Deal Sheet: a single shared record, created the moment two agents agree, that captures the CPM, the impression target, the flight dates, the format and the targeting in one place both sides sign. Through the campaign, every pacing signal and every amendment is written to that same record by both parties. At settlement there is nothing to reconcile, because the Deal Sheet is the invoice. The reconciliation step does not get cheaper. It stops existing.

That is the whole argument, so the cost it removes deserves precision. In the bilateral simulation, agents triggered 4,223 pacing interventions over 90 days. In the shared-record design, zero. One version of the bilateral market bolted a full reconciliation process on top, at a cost of $298,218.75 over the same 90 days. That spend bought exactly one thing: a clean reconciliation pass rate. It did not close the settlement gap, did not narrow the divergence between the two sides' records, and did not remove a single pacing intervention. In two of three seeds of the replicated run, because every correction is itself a new write, and every new write inherits the same small errors that caused the problem. Paying more to reconcile two wrong records did not make them right. It made them expensively wrong.

A fair objection: this is one firm's simulation of its own thesis, run on a controlled set of agents rather than the messy multi-model market actually coming. True, and worth separating into two kinds of number. The intervention count and the settlement gap are direct results of how the records were kept; they hold whatever agents you run. The market-scale projections carry more uncertainty, which is exactly why they are not the argument. The argument is structural, and it survives the caveat: when two sides keep their own books, the books drift, and no cleverness downstream undoes it.

Where the record lives

The whitepaper that reports these findings is deliberately silent on how to build the shared record. The structural finding holds whatever you build it on: the value is in the shared Deal Sheet, not in any one technology. That is the right call for a research document. It is the wrong call for an agency trying to decide whether this is real, so here is the part the paper leaves out.

Alkimi made its architectural choices after testing the options, and they are specific. The shared record runs on Sui.

A general-purpose blockchain is the obvious place a crypto-native team would reach, and mostly the wrong one. This is infrastructure, not ideology. Every market that clears real money at volume already runs on a shared settlement record; equities and derivatives built theirs decades ago, and nobody calls that exotic. Advertising is the outlier still keeping two sets of books. The reason most chains fail anyway is practical: they process transactions in a queue, which is fine for moving a token and useless for a market where thousands of unrelated deals are being negotiated and amended at machine speed. Sui fits because of how it handles data. Every object on Sui has a permanent unique identifier that is never reused. A Deal Sheet becomes one such object: a single addressable record, with one identity, that the buyer's agent and the seller's agent both write to directly.

The significance is what it removes. In a bilateral market, each agent writes to its own database. A rounding difference here, a timing difference there, and within days the two records of the same deal disagree by amounts nobody is checking. That is the entire mechanism behind the 677 million missing impressions in the simulation: not fraud, not bad agents, just two copies drifting apart in the dark. One shared object removes the second copy. There is one record, and a full history of who changed it and when.

Because every object declares upfront what it touches, the network can tell which deals are unrelated and run them at the same time. Your campaign's writes never wait in a queue behind someone else's. A market cannot ask deals to take a number.

The last requirement is speed of agreement. When negotiation happens at machine speed, a record that takes minutes to finalise is a record the agents have already moved past. Sui's consensus mechanism, Mysticeti, commits transactions in around 390 milliseconds, under half a second, and that finality is deterministic: once the network confirms, it is done, not probably done. The distinction sounds academic until an agent has to decide whether to act on a record it cannot yet fully trust. Deterministic finality means it never has to make that call.

“Sui's object model and consensus were designed with machine-speed markets in mind from day one,” said Adeniyi Abiodun, Co-Founder and Chief Product Officer at Mysten Labs. “When agents start transacting at the speeds and volumes Alkimi's research describes, you cannot have them waiting in a queue, and you definitely cannot have them acting on records that are only probably final. The infrastructure either fits the workload, or it gets in the way.”

The storage problem, and the one question agencies always ask

A deal record is too heavy and too sensitive to sit in the open on a public chain. The terms of a media deal are commercially confidential, and writing them to an immutable ledger is both expensive at programmatic volumes and, for any agency with a legal team, a non-starter.

The architecture splits the two jobs. The content of the deal, the terms a competitor would pay to see, is stored as an encrypted blob in Walrus, a Verifiable Data Platform, with an expiry you set. What goes on the chain is not the deal. It is a cryptographic signature of the deal: a hash that proves the record existed and has not been altered, and holds nothing commercially or personally sensitive in itself.

This is also the answer to the question every agency compliance lead asks inside the first ten minutes, the one that kills most blockchain pitches in the room. If a record is immutable, how does it survive GDPR's right to erasure?

“Walrus was built in anticipation of the explosion in agentic commerce that we all see coming,” said Kostas Chalkias, Co-Founder and Chief Cryptographer at Mysten Labs, original contributors to Walrus. “Agents represent a totally different set of demands on data infrastructure. From verifiability, to access controls you can programme. In addition to all the compliance needs of the teams that deploy them. Alkimi is operating at the bleeding edge of this space, and their research is proof of the step-change in performance the right infrastructure brings.”

It survives because the immutable part holds no personal data. When a deletion obligation lands, the encrypted blob is removed from the storage layer. This is not a compliance workaround bolted on after the fact. Walrus was built with deletion in mind: blobs, in the project's own whitepaper, "can be set as deletable by their writer" and removed with a single Sui transaction. The on-chain signature stays, because it cannot do otherwise, but it now points to nothing. What remains is a tombstone: cryptographic proof that a record once existed and was deliberately deleted, with no recoverable content behind it. The right to be forgotten is satisfied. The audit trail a regulator or a counterparty might separately demand is preserved. Data residency rules in specific jurisdictions are handled by controlling who can reach the storage layer. This is the rare case where the on-chain answer to a compliance question is stronger than the database answer, not weaker.

What this is not

Three quick clarifications, because the idea is easy to mistake for things it is not.

It is not a replacement for deal IDs. In PMP and programmatic guaranteed buying, a deal ID already gives both sides a shared reference, and the Deal Sheet does not compete with it. A deal ID confirms that both parties are pointing at the same inventory package. It does not record what was agreed on price, volume or pacing, and it has nothing to say about how those terms changed on day 57. The deal ID names the relationship; the Deal Sheet records the deal, which is what makes the relationship useful for the length of a campaign rather than only at the moment of activation.

It is not a speed pitch, and it is not impression verification. Sub-second finality matters because agents transact faster than people, not because fast is impressive on its own. Whether an impression was real and seen is a separate problem, handled elsewhere in the stack. This is strictly the record of what two parties agreed to buy and sell.

The market that compounds

Return to the agent that gets better with every deal. Once both sides write to one verified record, every closed campaign becomes a fact rather than a claim: this publisher actually delivered video at this CPM in this market, this structure actually paced cleanly, these terms actually settled without a dispute. A buying agent negotiating its next deal works from verified history instead of accumulated assumption. A selling agent prices to what buyers have paid, not to what they say they will pay.

Ben Putley, Alkimi's CEO and co-founder, makes the same point in commercial terms:

"Reconciliation has been treated as a cost of doing business for as long as I have been in this industry. It never was one. It was the price of two parties refusing to keep the same record. Take that away and the money stops leaking, and the agents start learning from fact instead of fiction. Really it is just capital becoming additive rather than extractive. And long overdue."

That is the advantage the bilateral market can never reach. Its history is contaminated by an unknown amount of drift, so its agents learn on sand. A market built on a shared record gets sharper every time it clears. And a record both sides trust supports instruments a bilateral market cannot: forward commitments, guaranteed-delivery structures priced against what actually delivered rather than against a promise. The gap between the two widens with every deal, quietly, in the same direction the contamination ran in the first simulation, only this time on the right side of the ledger.

The agents are already here. The negotiation works. The one layer still missing is the record they negotiate against, and that is now a question with an answer.

The technical specification is available to qualified partners as part of a structured pilot, which is the low-exposure way to test the claim against your own inventory before anything goes near a board deck. For the spec, marketing@alkimi.org. To scope a pilot, lauren@alkimi.org.